Insuring Against the Unknown: Navigating Uncertainty in the Geopolitical Environment

We live in a world that is increasingly interconnected by global flows of goods, services, capital, people and data, which are, in turn, dependent on political forces within the geographic space.

The recent geopolitical context has been heightened with shocks from events such as the COVID-19 pandemic and ongoing conflicts, in addition to continued technological competition and conflict tension between countries.

As market players, insurance companies worldwide inevitably feel the impact from such geopolitical risks, both in their capacity as businesses as well as providers of service, taking on the risks which have been transferred by policyholders. This brings about both challenges and opportunities for insurers.

Recent geopolitical events

To appreciate how insurers are potentially impacted by geopolitical risks, it is worth reflecting on notable international events in recent years.

In May 2020, the Joint Standing Committee on Foreign Affairs, Defence and Trade adopted an inquiry into the implications of the COVID-19 pandemic for Australia’s foreign affairs, defence, and trade. In its report, the Standing Committee comments on impacts of the pandemic on the global economy, including disruptions on the supply chain for labour and materials, foreign investments, cyber security, international relationships and potential trends towards global bifurcation[1].

The final point hints at continued strategic competition between the United States and China as both jurisdictions invest in technologies and other areas affecting trade and foreign investments.

Technological advancements and increased global usage also provide some context for growing concerns with cyber risks. Potential increases in cyberattacks and continued uncertainties regarding the coverage of cyber insurance policies are also heighted by recent geopolitical conflicts, in particular the Russia-Ukraine and Israel-Palestine tensions.

Climate risk and energy security have also been topical in recent years as extreme weather events and other climate change phenomenon become more prominent. These represent significant geopolitical risks which may contribute to issues including resource scarcity, food insecurity, population displacement, supply chain disruptions and infrastructure damage.[2]

In addition to these events, this year will see elections in over 50 countries. As such, there may be significant shifts in national and cross-border policies, as well as geopolitical relationships, which impact individuals and businesses. This may exacerbate or alleviate risks and introduce new geopolitical tensions.

Impact on insurers: Insurance businesses

Insurers are important societal players impacted by geopolitical circumstances on two fronts.

To begin with, insurance companies are businesses operating within an economic context, where changes in monetary and fiscal policies impact factors such as inflation and discounting, thereby leading to movements in the value of its assets and liabilities.

For instance, during the COVID-19 pandemic, many governments in advanced economies have funded major fiscal responses to the crisis by issuing government debt securities. Despite the increased issuance, interest rates paid on new government debt had declined.

Simultaneously, the central banks in these economies have also lowered their policy rates and made large-scale purchases of government bonds in secondary markets in pursuit of inflation and employment targets.[3] Such economic trends in response to the geopolitical circumstances of the time would have impacted the investment earnings of insurance businesses.

Furthermore, as part of managing the business, key internal stakeholders within insurance companies would need to consider the resilience of its operations, strategies and capital in light of potential geopolitical trends via mechanisms such as scenario planning.[4]

As part of this process, insurers may consider their exposures to ongoing geopolitical tensions should the current state persist or escalate, such as potential developments in malicious cyber activity, as well as a potential repetition of major geopolitical events such as the COVID-19 pandemic. These are just some examples of how insurers, as businesses, are impacted by the geopolitical context.

Impact on insurers: Insurance coverage

As providers of insurance products and services to individuals, businesses and the government, insurers are also exposed to the risks of others which have been transferred and agreed to be insured. That is, the policyholders’ exposure to geopolitical risk may be indirectly transferred to insurers.

Another key area that insurers may wish to watch out for is the wording of their insurance policy clauses, particularly whether the coverage and exclusions continue to reflect intended risk exposures within a shifting geopolitical context. For instance, the unprecedented nature and scale of the COVID-19 pandemic turned insurers and policyholders to judicial guidance in interpreting business interruption policy wordings.

In First Test Case, the High Court dismissed the insurers’ special leave application for appeal and the NSW Court of Appeal ruling under HDI Global Specialty SE v Wonkana No. 3 Pty Ltd [2020] NSWCA 296 remains. That is, insurers cannot rely on reference to the Quarantine Act 1908 (Cth) to deny liability in policies because that piece of legislation had been replaced by the Biosecurity Act 2015 (Cth). The Second Test Case focused on the interpretation of policy wordings on disease definition, COVID-19 outbreak proximity and the impact of government mandates.

The Full Court of the Federal Court of Australia ruled in LCA Marrickville Pty Limited v Swiss Re International SE [2022] FCAFC 17 and The Star Entertainment Group Limited v Chubb Insurance Australia Ltd & Ors [2022] FCAFC 17 that it is not unreasonable for insurers to withhold interest payments under s57 of the Insurance Contracts Act 1984 (Cth), which should be assessed on a case-by-case basis.

The High Court had largely upheld this decision but ruled that insurers cannot use JobKeeper payments to offset the insurance claim payouts if “savings” clauses were “in consequence” of the loss. Similar cases also took place in the United Kingdom.

The most prominent impact of this series of geopolitical uncertainty is that insurers with exposures to business interruption policies had set aside sizeable reserve provisions for COVID-19-related claims. These reserve allowances were then strengthened and/or released over time in response to the judicial rulings as well as evolvement of this geopolitical risk over time.

For instance, in November 2020, IAG had estimated a post-tax provision of $865m in light of the First Test Case.[5] Upon the High Court ruling on the Second Test Case in October 2022, IAG announced that it would reduce its COVID-19 business interruption provision by $360m.[6] The COVID-19 pandemic also demonstrates how geopolitical events may impact their risk exposure based on the interpretation of their policy wordings by the courts, which may inevitably be influenced by the overarching context. Evidently, it is vital that insurers regularly reflect upon how geopolitics may impact the interpretation of their existing contracts, in particular whether it is possible for unexpected liabilities to arise which had not been adequately reflected in the pricing. In this case, new exclusions/ updated wording may be required to clarify the scope of coverage as geopolitical circumstances change.

Impact on insurers: Trade and cyber

The economic situation is another topical issue which is inherently linked to geopolitics as the world becomes more interconnected through political engagements, cross-board trade competition and other means.

Many jurisdictions have experienced high inflations over the past few years, as driven by the out-workings of COVID-19 and supply chain disruptions, the Russia-Ukraine and Gaza conflicts and their respective consequences of trade, in addition to heightened political tensions globally. Central banks globally have responded to such an inflationary environment with movements in the cash rate, which in turn impacts the yield curve and has implications on discounting. This then impacts insurance reserving and pricing outcomes, in addition to the insurers’ investment portfolio.

Despite above discussions of geopolitical risks, there could also be opportunities for new types of insurance and/or insurance-like risk transfer mechanisms being realised as geopolitical situations continue to develop.

For instance, cyber insurance has a short history, tracing back to 1997,[7] with many jurisdictions still in comparative infancy compared to more mature products such as property and motor. Recent growth in offerings for cyber insurance has been catalysed by the growth in technology and data usage, partially driven by global competition for advancements, as well as exposures to cyberattacks which are often initiated from non-local criminal sources.

The largest multi-insured loss arising from cyberattacks to date is the NotPetya event in 2017, which has accumulated losses of over USD$3 billion. Countries such as the UK and US have accused Russia of being responsible for this event, but the latter has denied their involvement. Regardless of who is actually responsible, geopolitical tension is inevitably involved.

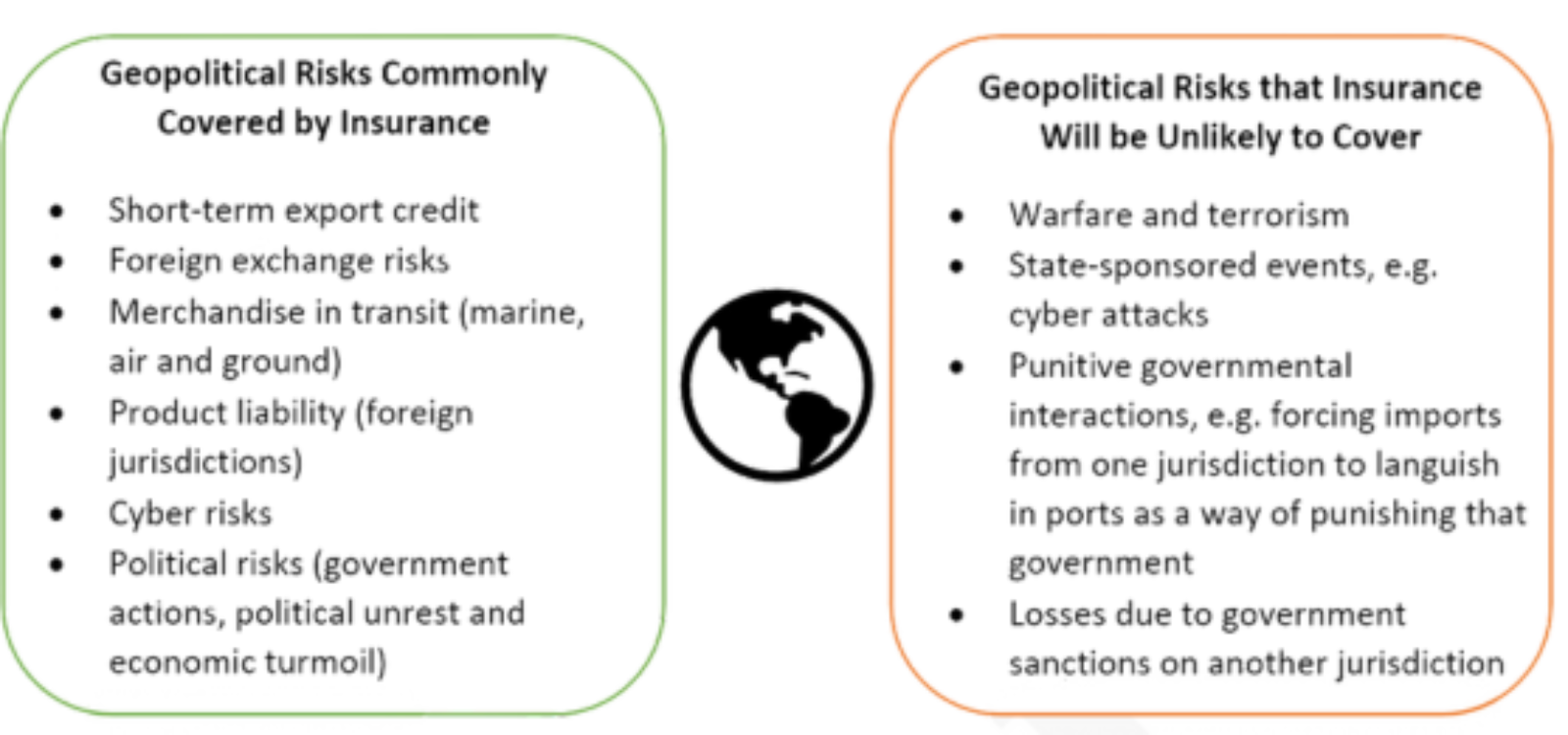

For more direct geopolitical risks, such as warfare and terrorism, insurers and/or individuals and firms with sufficient capital may not have the appetite to provide coverage. In fact, these are almost always excluded in insurance contracts. A potential reason is that providers may be perceived as “taking sides” between political powers, and therefore be subjected to unexpected risks in the future operations of the business in the other jurisdiction.

Even for less extreme geopolitical risks such as trade embargoes, most insurers may not have an appetite to provide direct coverage as explicit exposure to political actions may be undesirable. This is due to the fact that given policies are inherently unpredictable and dependent on the government of the day, as well as the relationships between relevant jurisdictions. Additional volatility is expected in 2024 with forthcoming elections across the world.

That said, trade insurance does exist to protect businesses engaged in international trade from risks associated with the export and import of goods and services across national borders. Larger market players such as syndicates of Lloyd’s of London provide for niche areas of coverage like this, where exposures are highly dependent on the geopolitical context.

For instance, Ascot Group provides for political risks covering physical assets which may be subject to confiscation, nationalisation, embargos, damage and other types of deprivation, as well as currency risks and inconvertibility, due to political destabilisation.

The coverage also protects policyholders from specified non-payments due to economic or financial distress in trade-related businesses, which may be due to the political situation of the time. Such coverage is targeted at financial institutes, export credit agencies and multilateral, rather than a jurisdictional government.[8]

Political risk insurance is particularly important for businesses conducting overseas trade in emerging economies, authoritarian countries, or both. Today, approximately 60 global insurers offer such coverage.[9]

Businesses doing cross-border trade: Are you covered?

All that being said, businesses engaged in international trade are most interested in whether their risks are being covered by insurance. A non-exhaustive list is provided below as a guide, but businesses should consult insurance experts to appreciate their unique risk exposures before engaging in overseas trade.

Looking forward

The geopolitical landscape creates both risks and opportunities for insurers around the globe in their capacity as businesses and service providers. Issues explored in this article may appear to have greater relevance for insurers with a global presence and/or coverage in locations that have recently been the subject of key geopolitical events.

Nonetheless, it is worth recognising that the world continues to be increasingly interconnected; impacts from global events such as the COVID-19 pandemic and supply chain outcomes arising from ongoing conflicts in Russia-Ukraine and Palestine-Gaza will inevitably flow onto local jurisdictions.

Moreover, while Australian insurers are predominantly focused on the local market, which itself is not at the forefront of geopolitical tensions, they are economically impacted as active businesses, in addition to the specifics of providing insurance services. From a prospective standpoint, it is also important to understand the potential impacts of existing geopolitical tensions should similar risks arise in the insurers’ own geographical realms of coverage in the future.

Businesses engaged in international trade are, to an extent, protected by a multitude of insurance categories including political risk insurance. However, growing geopolitical tensions in recent times, whether physical or financial, have coloured the landscape with uncertainty. These businesses should work towards ensuring that their unique exposures to geopolitical risk are sufficiently protected, whether through insurance or other means, to the extent of satisfying their risk appetites.

References

[1] Inquiry into the implications of the COVID-19 pandemic for Australia’s foreign affairs, defence and trade (aph.gov.au)

[2] Top Geopolitical Risks of 2023 | S&P Global (spglobal.com)

[3] Government Bond Markets in Advanced Economies During the Pandemic (rba.gov.au)

[4] Ignore geopolitical risk at your peril as tensions rise – Investment Magazine

[5] IAG responds to business interruption test case judgment and announces capital raising of up to $750 million to strengthen balance sheet | IAG Limited

[6] On-market share buy-back following conclusion of second Business Interruption test case | IAG Limited

[7] Cyberinsurance has been around for 25 years. It’s still a bit of a mess. (slate.com)

[8] Political-Risk-Appetite-Document.pdf (ascotgroup.com)

[9] Insurance and Geopolitics: Is Geopolitical Confrontation Making International Business Uninsurable? | American Enterprise Institute – AEI

CPD: Actuaries Institute Members can claim two CPD points for every hour of reading articles on Actuaries Digital.