Re-evaluating the ASFA Standard: How to Afford a “Comfortable” Retirement With Less Super

Do single homeowners really need $595,000 for a comfortable retirement and couples $690,000 as ASFA suggests?

We see and hear a lot of discussion in the press and elsewhere about how much money you need to retire. A popular method to help estimate this amount is the ASFA Retirement Standard.

For 20 years now, the Association of Superannuation Funds of Australia (ASFA) has been publishing a breakdown of the annual budget for a ‘comfortable’ or ‘modest’ retirement and the estimated super balance required to achieve it. This standard is widely used by super funds as a guide for their members and by commentators more generally.

But with the retirement landscape changing significantly in recent years, new retirement income products are emerging. In this article, we explore whether the new ‘lifetime’ income products can achieve the same comfortable retirement with less money.

ASFA Retirement Standard

The ASFA Retirement Standard estimates what lump sum super balance is required at age 67 to have a comfortable or modest lifestyle – assuming the retiree puts all their super into an account-based pension (or ABP). The calculations assume that the retiree draws down all their balance over time and receives a part Age Pension..

But how relevant is this approach today? Does the methodology remain appropriate, given that many retirees seem reluctant to spend all of their savings as they might “run out of money”? What about the growing range of new lifetime income products emerging to assist in this area?

These questions are especially relevant because people targeting the ASFA ‘comfortable’ lifestyle are likely to become eligible for a part Age Pension under means-testing rules. Here, lifetime income products can attract valuable incentives. For Age Pension purposes, only 60% of the income paid from a lifetime income product counts towards the income test. And, only 60% of the purchase price of a lifetime income product counts towards the assets test (up to age 84, or a minimum of five years. Thereafter only 30% of the purchase price counts).

Let’s take the example of a single homeowner. As of the date of writing, the most recent ASFA Standard (for the June quarter 2024) indicates that a single homeowner would need $52,085 per year to enjoy a comfortable lifestyle in retirement. To achieve this, ASFA estimates a 67-year-old would need a lump sum super balance of $595,000.

Is this lump sum calculation still appropriate?

If we take the ASFA figure of $595,000, we can project a retiree’s balance year by year throughout their retirement based on, say, a 6% per year net investment return. This allows us to explore how long their super will last, based on a living standard that costs $52,085 per year and keeps pace with inflation. It assumes they draw from their super account balance as required to fund this standard of living.

Note that with $595,000, the retiree will be eligible for some – but not all – of the Age Pension due to Centrelink’s means-testing rules. The income they get from the Age Pension reduces the amount they need to draw from super each year to spend $52,085 per year in total.

Assumptions:

- Single homeowner of average health

- No other savings or sources of income

- Uses an account-based pension for retirement with a 6% per year return (net of all fees and charges)

- Cost of living increases of 2.75% per year

- Increase in Age Pension payment rate of 2.75% per year

By placing their super into an account-based pension, over the course of retirement their balance is expected to reduce gradually as they spend it. This means that, under means-testing rules, the annual amount they’ll get from the Age Pension increases over time.

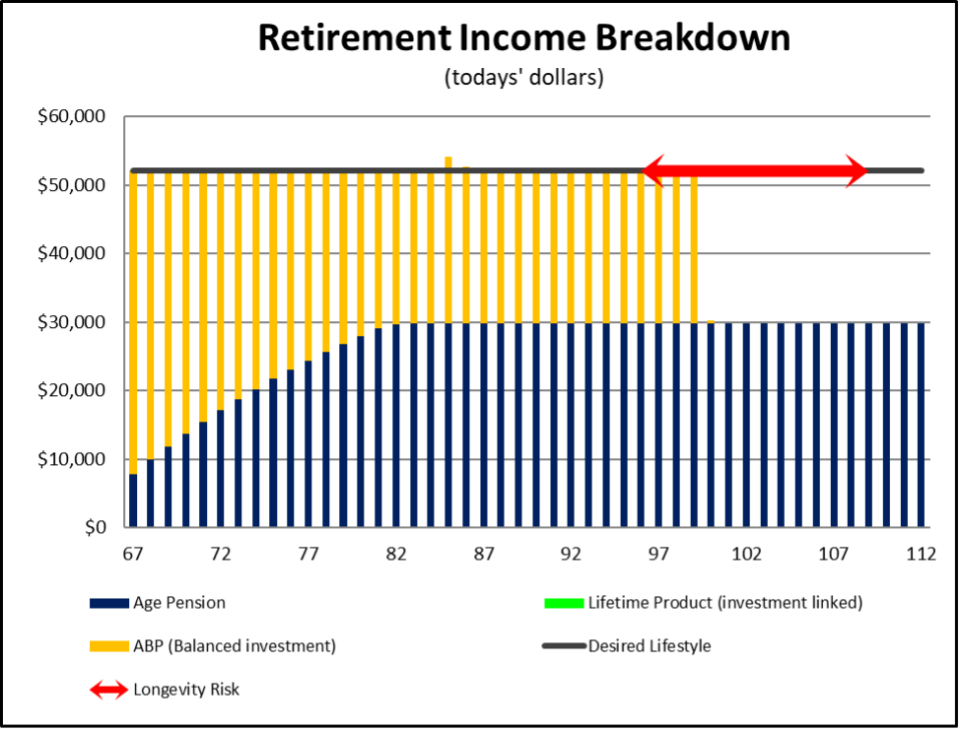

As you can see in Chart 1 below, the increasing payments the retiree receives from the Age Pension cover an increasing share of their total retirement spending. It means the annual amount they need to withdraw from their super balance will reduce while they still spend $52,085 each year. This is consistent with the lump sum calculation by ASFA.

Scenario 1: Current ASFA Standard using account-based pension only

(Lump sum super balance = $595,000)

All figures are in today’s dollars. The red arrow in the charts indicates longevity risk. One quarter of retirees are projected to live until somewhere within the ages indicated by the red arrow.

Chart 1 – Retirement Income Projection based on ASFA’s assumptions

The retiree’s balance, supported by income from the Age Pension, covers their spending right into the person’s late 90s. This projection assumes their super remains invested in an account-based pension and assumes their living costs and the Age Pension income both increase by 2.75% per year. The calculations allow for investment returns but ignore investment risk.

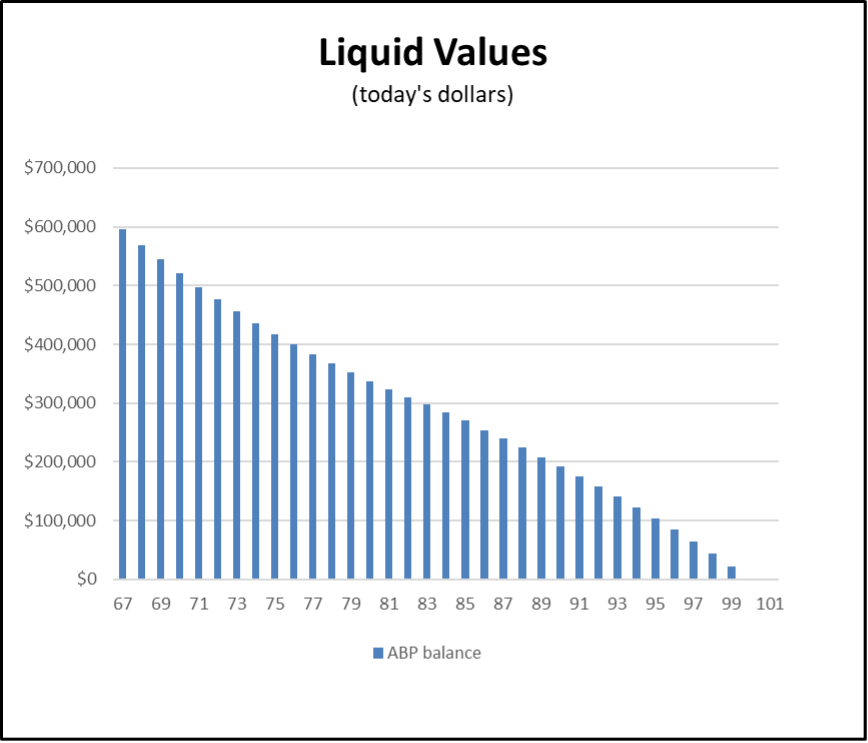

The following graph illustrates the reduction in the person’s projected super balance over the course of retirement if total spending equals the ASFA Comfortable Standard.

Chart 2 – Projected superannuation account balance based on ASFA’s assumptions

It’s important to note the projected balance has fallen significantly by the time they reach their 90s. The balance by age 94 falls to around $100,000 in today’s dollars. Most female 67-year-olds today are expected to live beyond age 90, and a quarter will live beyond age 95. Healthy, wealthier retirees tend to be in the longer-living groups and a growing number of Australians reach age 100 every year.

Account-based pensions do not protect retirees against longevity risk. This means it can be stressful to watch your super balance fall in the way ASFA assumes it does. It’s important to note that if returns are lower than the projected 6% (including the risk of negative returns) or inflation is higher, then the balance will run out sooner.

ASFA’s calculation might seem reasonable at first. However, there has been a significant government push to improve the retirement phase of superannuation in Australia. We now have an expanding range of ‘lifetime’ retirement products available to assist with turning superannuation into income. The above approach may therefore no longer be sufficient on its own.

What happens if your super balance is invested in a ‘lifetime’ income product?

The basis for ASFA’s calculation is to draw down from an account-based pension – which is the most common option that super funds provide for their retired members.

The 2014 Financial System Inquiry and the 2020 Retirement Incomes Review observed and concluded that putting some of a retiree’s balance into a lifetime income product could deliver 15% to 30% higher retirement income. This is achieved by trading often substantial super death benefits paid to beneficiaries from the ABP for a higher retirement income that lasts for life. Remember that each of us has only one life and we need a reasonable income to enjoy life.

Some life insurers and several super funds now offer lifetime income options in retirement and others are working on developing them. Apart from the appeal of income that is guaranteed to continue for life, lifetime income solutions also come with Age Pension incentives that can be especially valuable for retirees who are impacted by means testing – notably those aiming for the ASFA Comfortable Standard.

How to live comfortably on less super

Let’s look at an example to show how retirees can achieve ASFA’s comfortable retirement income with a lower lump sum than ASFA currently recommends, while receiving a higher retirement income from super and a higher Age Pension.

Consider what happens if our retiree (let’s call her Amy – a single homeowner) moves half her super into a new investment-linked lifetime pension or annuity. Based on current market rates, this product might pay Amy a starting level of annual income that is 5.4% of the amount she invests[1]. This is based on an ‘investment-linked’ design that passes on investment returns (up or down) but guarantees to keep paying income for as long as she lives. The income in this example is expected to increase over time, on average, a little more than inflation.

Good to know

The starting rate of income from a lifetime product is a function of the product’s design. A key feature is what increase rate will apply to the income in future. Products that increase income more rapidly tend to have lower starting incomes than products under which the income increases more slowly or doesn’t increase. Fully guaranteed products tend to have lower starting incomes than products that pass on most of the investment performance to customers.

If Amy has $595,000 in super and invests half ($297,500) into the above lifetime income product it could result in an annual income of $16,100. This is in addition to her Age Pension income and income from the remainder of her super (assumed to go into an account-based pension).

Only 60% of the lifetime product counts toward the means tests, which means her Age Pension increases from $7,836 in the first year to $17,118 now!

The fact that Amy receives a higher Age Pension plus the income from her lifetime product means she doesn’t need to draw as much from her remaining super balance to enjoy a lifestyle of $52,085 per year. In fact, based on investing $595,000 in this way, for most of her retirement, Amy’s income would be higher than $52,085. Even if she lives to age 104, she would still have some money in super, plus be receiving a combined income of $24,370 per year from the lifetime product and super as well as receiving nearly a full Age Pension.

Using a lifetime pension dramatically reduces risks to the sustainability of Amy’s income as a larger share of her income continues for life.

Does Amy still need $595,000 for a ”comfortable” retirement?

No. By using a lifetime income product, Amy can achieve the ASFA Comfortable living standard with a lower lump sum super balance at retirement.

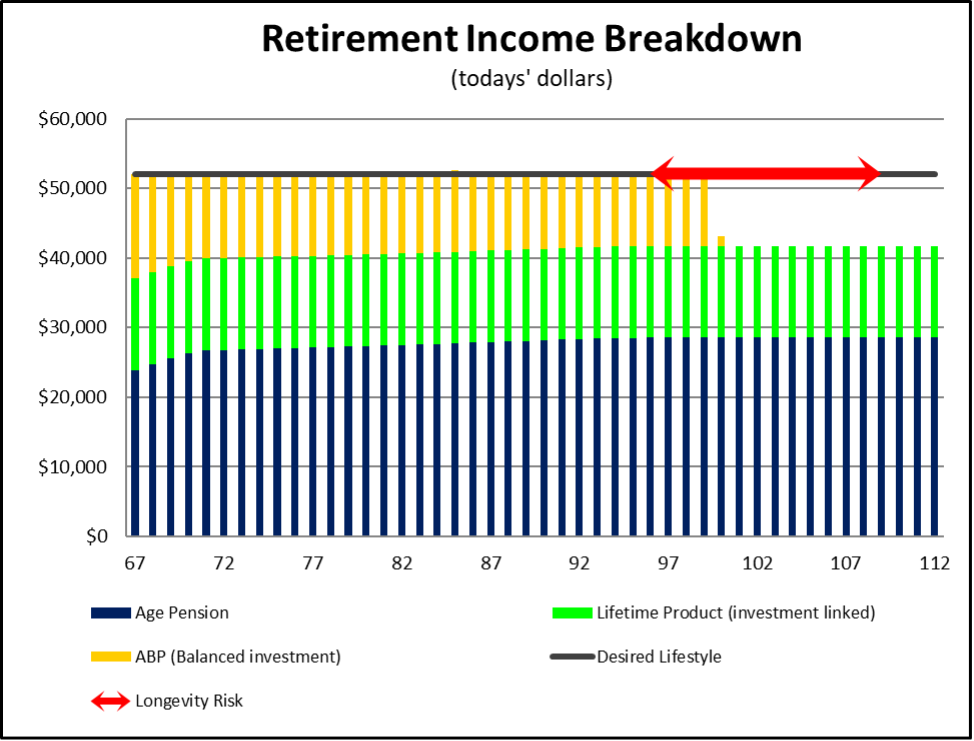

Suppose we re-work ASFA’s calculations by assuming 50% of her lump sum goes in a lifetime product.

Chart 3 below shows Amy can still achieve the ASFA comfortable lifestyle to age 99 with a lump sum balance of only $488,000. That’s over $100,000 less than ASFA’s recommended target and her remaining ABP is projected to last to the same age as ASFA’s approach in Chart 1. It takes significant pressure off the amount Amy would need to save during her working career. It may even mean she can retire earlier than if she was trying to save $595,000.

Scenario 2: Potential ASFA Standard (Lump sum super balance = $488,000)

Chart 3 – Retirement Income Projection with 50% in a lifetime product

Amy’s retirement income is also more sustainable as the lifetime product’s income continues for as long as she might live and isn’t subject to sequencing risk in the same way that an account-based pension is. It cannot run out. She has substantially reduced her “longevity risk”.

Sequencing risk refers to the order in which investment returns occur. If markets fall at a time when you are making withdrawals from an investment, then it means you’re withdrawing when values are down. It can mean having to sell assets at low values in order to pay that withdrawal. This is especially problematic with account-based pensions because once that money is withdrawn, it can’t recover again when markets rise again. Investment-linked lifetime products do not suffer from this because when markets recover the full income level benefits accordingly. Read more about sequencing risk.

Summary

Encouraging people to save more for retirement is a worthwhile objective. The more money people put into super, the better their lifestyle could be, but this comes at a cost to their lifestyle during their working years. It may also mean people work for longer than they need to.

By using lifetime income products, ASFA and super funds can recommend a lower, safer target and at the same time help reassure more people that a comfortable retirement may not be out of their reach. In so doing, Australians may be able to achieve the ASFA Comfortable living standard with a significantly lower lump sum super balance than the published figure today. Conversely, they may be able to achieve a higher retirement income from the same amount of super. They can also enjoy a higher degree of confidence that their savings won’t run out as their “longevity risk” is reduced.

Similar results can apply to couples in retirement. As of the date of writing, ASFA’s suggested superannuation balance for a 67-year-old couple to enjoy a comfortable retirement (spending $73,337 per year) is $690,000. By allocating 50% of their superannuation to a lifetime product and using similar assumptions, they could achieve the ASFA comfortable lifestyle to age 99 but with a lump sum balance of only $570,000. That’s over $100,000 less than ASFA’s recommended target.

Good retirement strategies must help retirees to make informed trade-offs – deferring consumption now for consumption in later years – rather than just achieving the maximum balance and “funds under management”.

References

[1] Based on an investment-linked annuity design provided by Generation Life with a 2.5% ‘lifebooster’ rate. The 2.5% means a higher level of starting income gets paid in return for indexation being the net return less 2.5%. Refer to “What is an investment-linked annuity” for information about this product category.

CPD: Actuaries Institute Members can claim two CPD points for every hour of reading articles on Actuaries Digital.